Worried About Inflation? Real Estate May Be One of the Best Long-Term Hedges

Published on May 21, 2026 by

Stephanie Younger

Inflation does not just raise prices. It quietly erodes purchasing power.

Since 2020, consumer prices have risen dramatically, meaning the same dollar buys meaningfully less today than it did before the pandemic. That is one reason many buyers feel like home prices have moved impossibly far out of reach. Part of the story is rising real estate values. But another major part is that the dollar itself has weakened.

That is why real estate remains one of the most important long-term inflation hedges, especially in supply-constrained markets like Los Angeles.

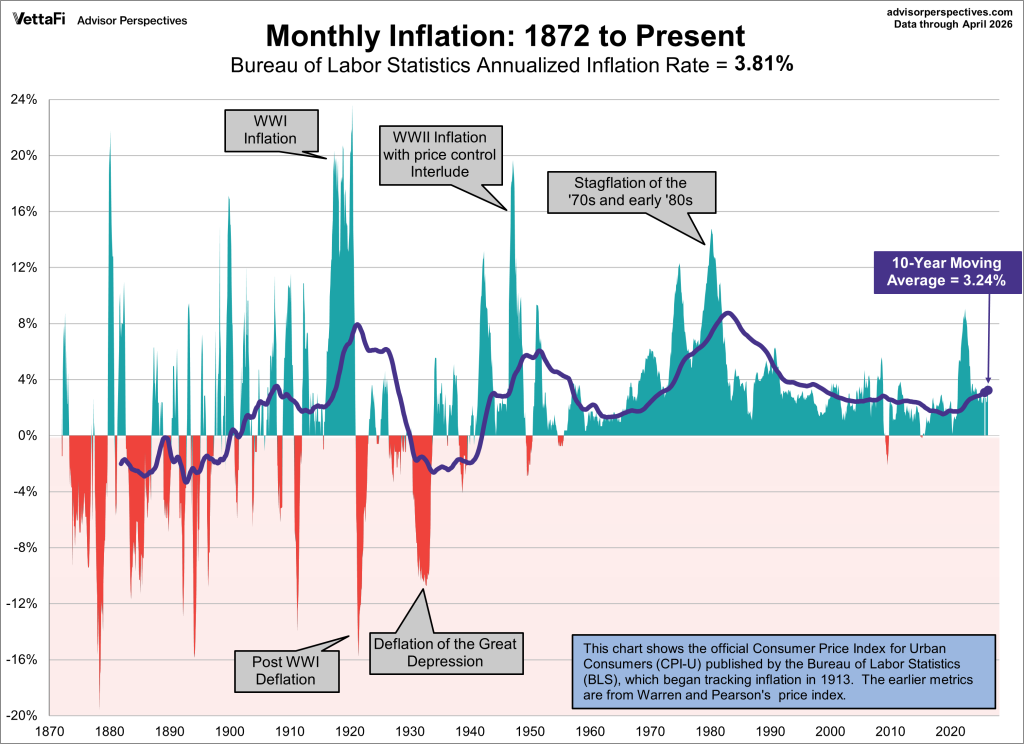

Many economists and investors increasingly compare today’s environment to the 1970s because several major forces look surprisingly similar:

In the 1970s, inflation remained elevated for years longer than many expected. Interest rates rose sharply as the Federal Reserve attempted to contain inflationary pressures tied to energy shocks and economic expansion.

Today, the economy is once again experiencing:

While history never repeats perfectly, many analysts believe the coming decade could look structurally more similar to the inflationary 1970s than the ultra-low-rate environment of the 2010s.

Real estate tends to perform well during inflationary periods because:

and fixed-rate mortgage debt becomes cheaper in future inflated dollars.

In other words, when inflation pushes the cost of everything higher, well-located real estate often rises alongside it.

This is especially true in Los Angeles, where housing supply remains structurally constrained. The city continues facing:

At the same time, demand continues growing from:

The 1970s were marked by inflation, oil shocks, and high interest rates. Many buyers hesitated because borrowing costs felt painfully expensive.

But homeowners who purchased real estate during that decade were often rewarded substantially over time.

National median home prices nearly tripled between the early 1970s and 1980. The lesson was simple:

High interest rates did not stop inflation-driven asset appreciation.

In many cases, waiting became more expensive than buying.

A $5 million average Los Angeles home price sounds extreme today. But over a 30-year period in a persistently inflationary environment, it is not impossible.

That is not a prediction. It is a scenario illustrating how compounding inflation and constrained supply can reshape pricing over decades.

Of course:

But homeowners with appreciated equity may be far better positioned to “climb the property ladder” than renters starting from scratch in future, inflated dollars.

Many renters today are experiencing a difficult reality:

Their monthly rent may still feel cheaper than today’s mortgage payment, but the home they want keeps moving further away.

As prices rise:

This is why real estate has long been viewed as a long-term wealth preservation strategy. Your first property does not need to be your forever home. It becomes an asset that helps you move into the next one later.

Without ownership, buyers may eventually face severe sticker shock trying to purchase future assets using depreciated dollars.

California sits at the center of the global AI revolution.

Massive investment into:

It is creating enormous economic expansion throughout California.

That spending creates jobs, wage growth, and housing demand — especially across coastal Los Angeles communities tied to technology and aerospace employment.

At the same time, Los Angeles is not building enough homes to offset future demand meaningfully.

That imbalance may continue placing upward pressure on housing prices for years to come.

Higher interest rates make housing feel expensive today.

But inflation can make waiting expensive in an entirely different way.

For long-term buyers, real estate remains:

If the next decade resembles the inflationary environment of the 1970s more than the low-rate environment of the 2010s, real estate may once again prove to be one of the strongest long-term wealth preservation tools available.