One Key Sign We’re Not Headed for a Wave of Foreclosures | Stephanie Younger Group

Sign Up

for news & updates

Get the latest insights delivered to your inbox.

We respect your privacy and reach out thoughtfully.

Main Content

One Sign We're Not Headed for a Wave of Foreclosures

If you've been following the news lately you've probably seen the headlines. Foreclosures are rising. If you've owned a home in Los Angeles long enough to remember 2008 that kind of headline probably stopped you mid-scroll.

We get that reaction. The last housing crash really hurt this city. Neighborhoods, families and the way people think about estate. So when foreclosure numbers start climbing, a little it's natural to wonder if we're heading down that road again.

Here's the thing though. We're not. The data is clear about why.

The Number Worth Actually Watching

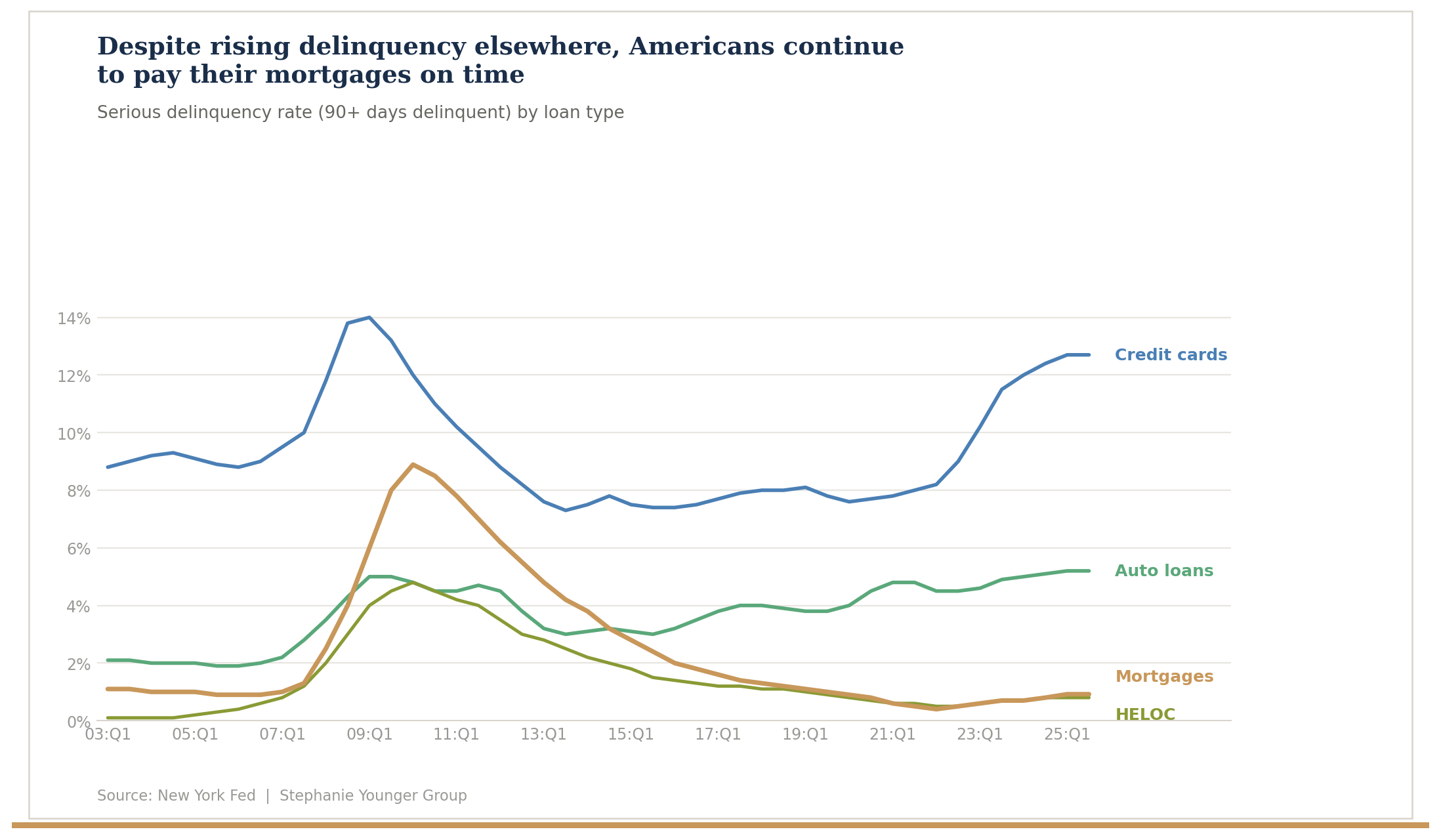

Foreclosure filings get a lot of attention. They're actually a late-stage indicator. By the time a home formally enters the foreclosure process a lot has already happened. The useful number to track is serious delinquencies. Homeowners who are more than 90 days behind on their mortgage. Think of it as the warning system.

Right now that early warning system is not going off. According to the New York Fed serious delinquencies have edged up slightly. They're still at historically low levels.

- Today 1 in 100 mortgages is seriously delinquent.

- Around the time of the 2008 crash it was closer to 1 in 11.

That's a difference. Los Angeles felt that crisis in a way. Prices dropped sharply neighborhoods stalled and the ripple effects lasted years. The numbers we're seeing today don't look anything like the lead-up to that period.

Falling Behind Doesn't Automatically Mean Losing Your Home

Something to keep in mind: even homeowners who do fall behind on payments don't automatically end up in foreclosure. Lenders have incentives to work something out.

- Repayment plans

- Loan modifications

- Forbearance agreements

Nobody wins when a neighborhood fills up with properties. Lenders know that well as anyone.

The result is that actual foreclosure activity is even lower than the delinquency data would suggest.

- ATTOM currently puts the share of homes in foreclosure proceedings at around 0.3% nationally. And a good chunk of those won't result in a completed foreclosure anyway.

That's not a wave rolling toward the LA coastline. That's a ripple.

When Money Gets Tight People Protect Their Homes First

Heres something that tells you a lot about where things stand. When household budgets get squeezed. And plenty of LA families are feeling that squeeze now between the cost of living and broader economic uncertainty. People have to make choices about which bills get paid.

Almost universally, the mortgage comes first.

New York Fed data shows that delinquency rates have climbed noticeably on credit cards and auto loans compared to home loans.

For people their home isn't just a financial asset. It's where their kids grow up where they've built their life. People will cut subscriptions dining out and discretionary spending before they miss a mortgage payment.

And Then There's the Equity Factor. Which Changes Everything

If theres one thing that truly separates todays market from 2008 it's this: most homeowners are sitting on equity. In Los Angeles, where values have appreciated substantially over the past several years that's especially true.

During the crash a huge number of homeowners across LA were underwater. Meaning they owed more on their mortgage than their home was worth.

Today the picture looks very different.

- Daren Blomquist of Auction.com noted that many distressed homeowners now still have equity on their side. Which means they have real choices.

They can sell on their terms pay off what they owe and walk away without losing everything.

What Does This Mean for LA Homeowners Now?

It means the headlines deserve a little skepticism. Not dismissal, but context.

Yes foreclosure activity is ticking up. That's worth monitoring.

The underlying conditions that turned a rise in delinquencies into an all-out crisis in 2008 aren't present in todays market in the same way.

Los Angeles real estate has always been resilient. That doesn't mean it's immune to pressure. It doesn't mean every homeowner is in a comfortable spot right now.

The data points to a market that is adjusting, not unraveling.

For most homeowners in West LA the fundamentals are still working in your favor.

Bottom Line

- Foreclosures are rising slightly.

- They are not rising in a way that resembles the lead-up to a crash.

- Serious delinquencies are a fraction of what they were in 2008.

- Homeowners are prioritizing their mortgage payments over debt.

- The equity most people have built gives them flexibility if things get harder.

The smartest thing you can do now isn't panic. Its stay informed.

If you're wondering what any of this means specifically for your home or your situation here in LA that's exactly the kind of conversation we love to have.

Reach out to the Stephanie Younger Group anytime.

We're always happy to talk through what the market's actually doing. And what it means for you.

Find out what your home is worth →

Talk to us about buying on the Westside →

The Stephanie Younger Group | Compass | Los Angeles

Data referenced from the Federal Reserve Bank of New York ATTOM Data Solutions and Auction.com. Figures reflect conditions as of 2026.

More From Our Blog

Social Media

Follow

on Instagram

on Instagram